While everyone watches the rockets, a different set of companies is quietly building the infrastructure layer that all lunar missions depend on.

By Rabbt | May 11, 2026

In April 2026, humans traveled around the Moon for the first time since 1972.

NASA’s Artemis II mission completed its crewed lunar flyby, generating enormous coverage, stunning photographs, and genuine public excitement about the future of space exploration.

But most of that coverage missed the point.

Artemis II was not designed to land on the Moon. It was a systems test. NASA needed to validate deep-space navigation, life support, crew operations, and communications infrastructure before future lunar landings begin. The mission answered one question: do our systems work at this distance?

The answer was yes. Which means the next question is already being asked: what do we build now that we know we can get there?

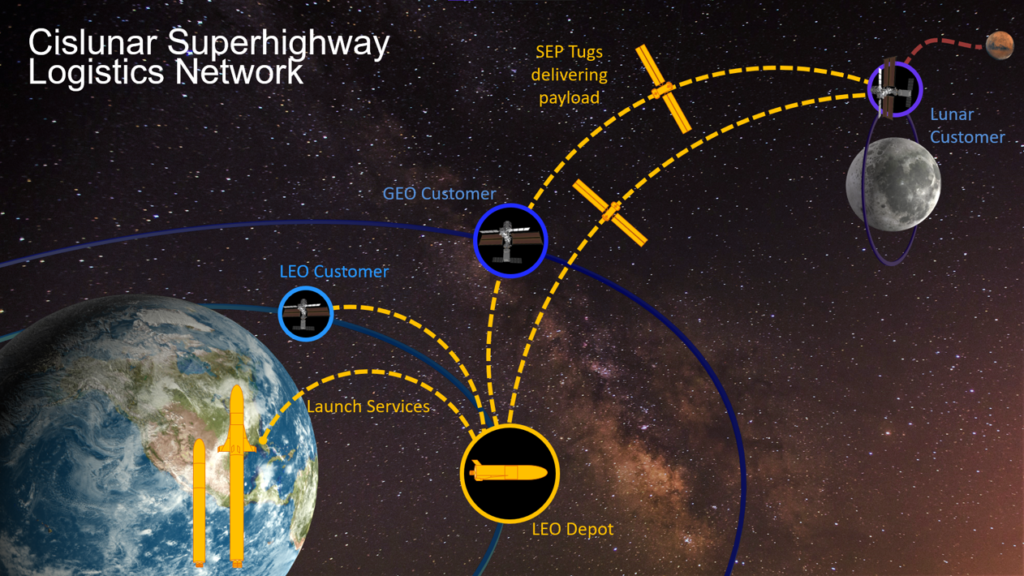

That shift, from “can we reach the Moon” to “what do we build there,” is the most important story in the space industry right now. The companies best positioned to answer it are not necessarily the ones building the biggest rockets. They are the companies building the invisible infrastructure underneath the missions: navigation, communications, power, cargo, and robotics.

| Want more Frontier Economy intelligence? Follow the research as it develops. Subscribe to Rabbt on Substack at rabbt.substack.com. |

Why This Moment Is Different From Apollo

Apollo was a geopolitical demonstration. The United States needed to reach the Moon before the Soviet Union, and once it did, the program wound down. Thirteen missions. Twelve men on the surface. Then nothing for fifty years.

Artemis is being designed around a fundamentally different goal: permanence. NASA has openly discussed plans for a long-term lunar base, sustainable surface operations, and eventually the extraction and use of lunar resources. The agency’s stated goal is not to visit the Moon. It is to stay.

Once governments start building permanent infrastructure somewhere, private industry historically follows. Railroads. Internet backbones. Cell towers. Cloud computing. The Moon may become the next infrastructure layer, and that changes the economics for every company involved.

What the Lunar Economy Actually Needs

Before a single permanent crew can operate on the Moon, an enormous amount of infrastructure has to exist. Consider what basic Earth operations require, then imagine building all of it from scratch: 240,000 miles away, with no atmosphere, extreme radiation, temperature swings of 500 degrees Fahrenheit, and no existing supply chains.

- Navigation systems that work in lunar orbit and on the surface

- Communications relays that keep surface crews connected to Earth

- Power generation that survives lunar nights lasting two Earth weeks

- Cargo landers that reliably deliver equipment to precise landing zones

- Robotics capable of operating autonomously without real-time human control

- Orbital logistics platforms to support crew transit and resupply

- Resource extraction systems for water ice, minerals, and regolith

None of those things exist yet at commercial scale. Every single one represents a business opportunity. The companies that establish early positions in any of those categories could become foundational suppliers for everything that follows. This is the picks-and-shovels dynamic. During the California Gold Rush, the people who consistently made money were not the miners. They were the ones selling the shovels, the boots, the food, and the logistics.

Four Companies Worth Understanding

Intuitive Machines (Ticker: LUNR)

Ticker: LUNR Price: ~$28.97 Market Cap: ~$6.3B 52-Week Range: $7.78 to $31.15 2026 Revenue Guidance: $900M–$1B

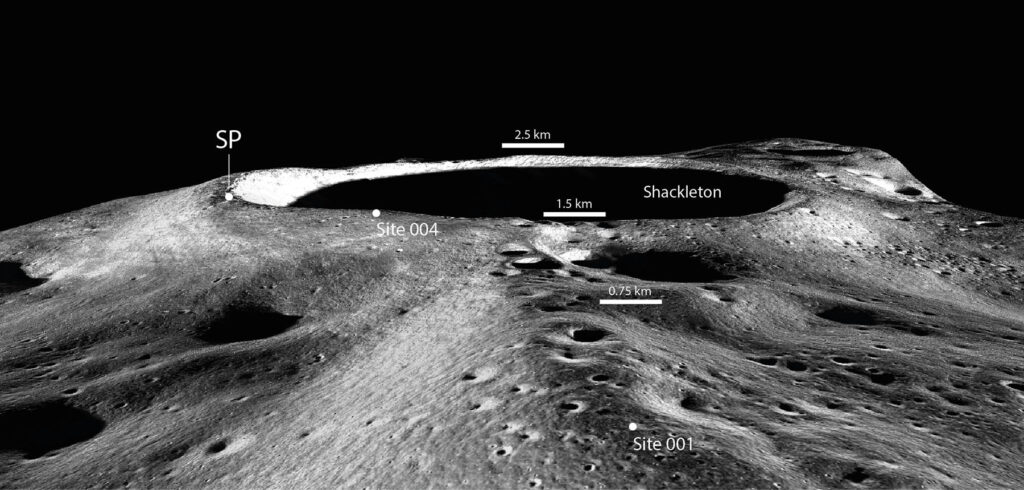

If Artemis is the highway to the Moon, Intuitive Machines is positioning itself as the company that runs the cargo network. Through NASA’s Commercial Lunar Payload Services program, known as CLPS, Intuitive Machines has become one of the agency’s most important commercial partners for delivering hardware to the lunar surface. In March 2026, the company received a $180.4 million contract for a mission delivering infrastructure and scientific payloads near the lunar south pole.

The south pole is not a random destination. It is the most strategically important region on the Moon. Permanently shadowed craters there are believed to contain water ice, which can be processed into drinking water, oxygen for life support, and hydrogen and oxygen for rocket fuel. Control over lunar south pole resources could eventually mean something like control over the Moon’s refueling infrastructure.

Intuitive Machines is not simply building landers anymore. Its long-term roadmap includes communications relays, surface navigation systems, and what may eventually function as a permanent logistics presence near the south pole. Additionally, its recent acquisition of Lanteris Space Systems supports a revenue trajectory that management has guided to $900 million to $1 billion for 2026. However, the company is not yet profitable, and government contract dependence remains the primary structural risk.

What to Watch: Earnings on May 14, 2026. Whether Intuitive Machines converts its CLPS contract wins into a second commercial customer outside NASA. The first signed non-government lunar logistics deal would signal a structural shift.

Rocket Lab (Ticker: RKLB)

Ticker: RKLB Price: ~$117.72 Market Cap: ~$67.8B 52-Week Range: $20.23 to $120.30 Q1 2026 Revenue: $200.35M (+64% YoY)

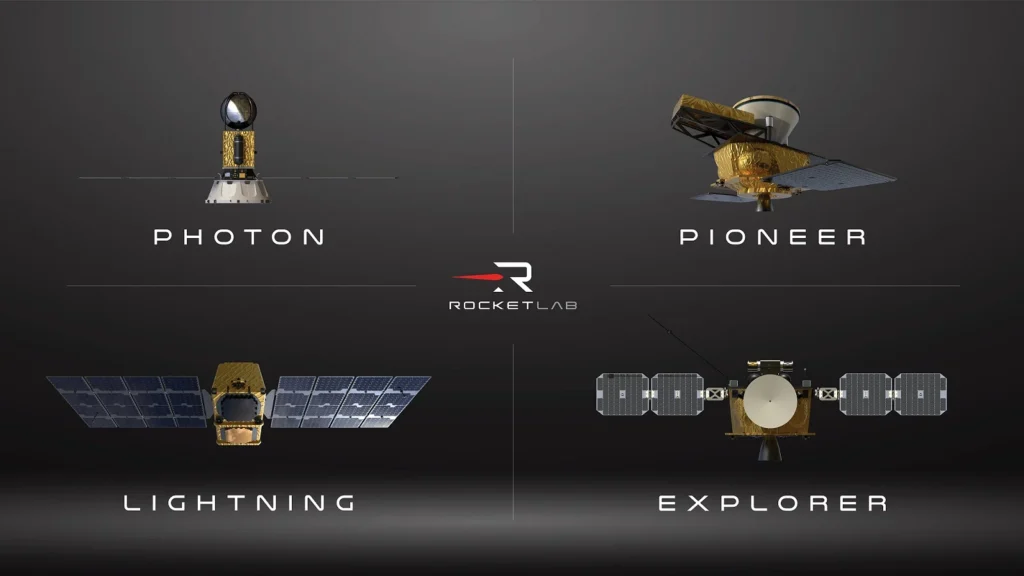

Most people still think of Rocket Lab as a launch company. That view is becoming significantly outdated. Over the past several years, Rocket Lab has been systematically transforming itself into something closer to a vertically integrated space industrial manufacturer. Its Space Systems division produces satellites, spacecraft components, solar power systems, guidance systems, communications hardware, and space robotics, which is the full stack of hardware that modern space missions require.

The company’s contract backlog has grown to approximately $2.2 billion, a figure that reflects the breadth of its manufacturing operations rather than simply launch contracts. Its upcoming Neutron rocket, designed for medium-lift missions, could expand the company’s addressable market significantly. Additionally, Rocket Lab recently completed the Mynaric acquisition, adding laser optical communications to its growing space systems portfolio, which is directly relevant to lunar infrastructure.

What to Watch: Whether Neutron delivers on its medium-lift promise. Any Lunar Gateway or cislunar infrastructure contracts would validate the thesis that Rocket Lab is becoming the industrial backbone of the Artemis ecosystem.

Redwire Space (Ticker: RDW)

Ticker: RDW Price: ~$12.19 Market Cap: ~$2.4B 52-Week Range: $4.87 to $22.25 Q1 2026 Revenue: $96.97M (+58% YoY)

Redwire may be the least-known name on this list among general readers, but inside the Artemis contractor ecosystem it is quietly important. The company builds solar arrays for spacecraft, space manufacturing systems, robotics, avionics, and autonomous systems for orbital operations. In 2026, it added a quantum-secure satellite communications contract with the European Space Agency alongside new solar array contracts.

Its solar technology deserves specific attention in the context of the Moon. The lunar environment is genuinely hostile: temperature swings exceeding 500 degrees Fahrenheit between day and night, radiation exposure with no atmospheric protection, and lunar nights that last approximately two Earth weeks. Any sustained surface operation requires power systems that can survive those conditions reliably. Redwire also holds a record backlog of $498.1 million as of Q1 2026, reflecting strong demand despite a Q1 earnings miss.

What to Watch: Whether the ESA quantum-secure satellite contract generates a second international defense or civil space win. Full-year revenue guidance of $450M–$500M requires consistent execution through the remainder of 2026.

SpaceX (Private)

No honest survey of the Artemis ecosystem leaves out SpaceX, even though it is privately held and not directly accessible to most public market investors. NASA selected a lunar variant of SpaceX’s Starship as the Human Landing System that will carry astronauts from lunar orbit to the Moon’s surface for future Artemis missions. That selection makes SpaceX structurally essential to NASA’s program in a way no other single company currently is.

The more interesting long-term question is not simply whether Starship reaches the Moon. It is whether SpaceX becomes the dominant logistics layer for the entire cislunar economy, the space between Earth and the Moon, the way Amazon became the logistics layer for internet commerce. SpaceX has reportedly filed confidentially for an IPO targeting a valuation above $2 trillion, which may eventually create public market access. However, for now, its structural importance to this ecosystem is context, not an actionable position.

Comparison: Lunar Infrastructure Stack Positions

| Company | Role in Stack | Structural Position | Key Dependency | What to Watch |

| Intuitive Machines (LUNR) | Cargo landers, surface logistics | Controls surface delivery for NASA CLPS; building toward permanent logistics presence at lunar south pole | Dependent on NASA contract renewals and CLPS program continuity; Lanteris acquisition integration risk | Earnings May 14, 2026; first non-NASA commercial lunar logistics contract |

| Rocket Lab (RKLB) | Launch, space systems manufacturing | Vertically integrated manufacturer supplying components across the stack; backlog $2.2B covers launch and space systems | Neutron rocket delivery timeline; dependent on continued defense and civil space contract flow | Neutron first launch; any cislunar or Lunar Gateway manufacturing contract win |

| Redwire Space (RDW) | Solar arrays, robotics, orbital manufacturing | Supplies power systems and robotics that every sustained lunar operation depends on; early position in orbital manufacturing | Q1 earnings miss signals execution risk; dependent on aerospace prime contractors as customers | Second major international contract win; progress toward full-year $450M–$500M revenue guidance |

| SpaceX (Private) | Crew and cargo transportation to lunar orbit and surface | Structurally essential as the Human Landing System for Artemis; only company with Starship HLS selected by NASA | Starship technical milestones and NASA program budget continuity | IPO timeline; Starship HLS crewed lunar landing demonstration |

How to Think About the Risk

It would be irresponsible to describe these companies without being direct about what could go wrong. Government programs slip. Budget cycles shift. Technical challenges cause mission delays measured in years. Several companies in the broader space sector have struggled with the gap between government contract revenues and the path to commercial profitability.

The companies worth watching long-term are the ones demonstrating actual hardware delivery, growing contract backlogs, and a credible path to recurring commercial revenue, not just government mission wins. Intuitive Machines has delivered hardware to the lunar surface. Rocket Lab has a large and growing manufacturing operation with record Q1 revenue. Redwire has multiple active international contracts. That is a different category from companies with compelling presentations and no flight hardware. The distinction matters.

Beyond individual execution risk, the broader bet here requires sustained government investment over a decade or more. If Artemis funding contracts significantly, every company on this list is affected. That is the structural dependency that sits above everything else.

The Apollo era is remembered for the astronauts. The Artemis era will probably be remembered for something less photogenic but more durable: the infrastructure that made sustained human presence on the Moon possible. Navigation. Communications. Power. Cargo. Robotics. The systems that no single mission can survive without.

The rockets get the headlines. The infrastructure companies may build the real economy. And for the first time in fifty years, that economy is no longer theoretical. The contracts are being signed. The hardware is being tested. The missions are flying. The question is no longer whether the Moon economy begins. The question is who builds the foundation it stands on.

| Rabbt Intelligence Note A structured Research File on Intuitive Machines would map its CLPS contract dependency against the evidence of repeat mission hardware delivery, and flag the first signed non-government commercial lunar logistics contract as the change trigger most likely to shift this picture from government-dependent operator to independent lunar infrastructure utility. The Relationship Graph would show that Rocket Lab sits inside the Artemis supply chain as a component supplier to missions Intuitive Machines operates, creating a structural connection between two separately traded companies that most coverage on either misses entirely. The open question: does the permanent lunar south pole presence Intuitive Machines is positioning toward require a second government commitment beyond NASA before it becomes a financially durable model? |

0 Comments