Interlune and the First Real Lunar Resource Economy

The purchase orders are signed. The NASA contract is awarded. The customers are named. The question is no longer whether a lunar resource economy can exist. It is whether this supply chain can actually deliver.

By Rabbt | May 29, 2026

The U.S. Department of Energy has agreed to buy three liters of helium-3 from the Moon. That sentence is not science fiction. It is a binding purchase agreement, and it is the first documented government purchase of a non-terrestrial natural resource in history.

Most coverage of this moment treated it as a curiosity. The structural reality is different. When the DOE’s Isotope Program commits to a delivery, however small the volume, it is establishing a legal and commercial precedent for how lunar resources get purchased, priced, and received. The DOE contract does not exist in isolation. Bluefors, the world’s largest manufacturer of dilution refrigerators, has committed to purchasing up to 10,000 liters of lunar helium-3 annually from 2028 to 2037. Maybell Quantum has committed to annual deliveries from 2029 to 2035. Together with additional agreements, Interlune reports nearly $500 million in binding purchase commitments. The frontier economy does not typically see that kind of forward demand before the first unit has been extracted.

Why Helium-3 and Why Now

Helium-3 is not abundant on Earth. Nearly all terrestrial supply comes from the radioactive decay of tritium in nuclear weapons stockpiles, primarily in the United States. That process is slow, the stockpiles are finite, and the production rate does not scale. The structural deficit, based on current estimates, runs to roughly 20,000 to 40,000 liters per year: demand already exceeds terrestrial supply, and that gap is growing as quantum computing scales toward industrial deployment.

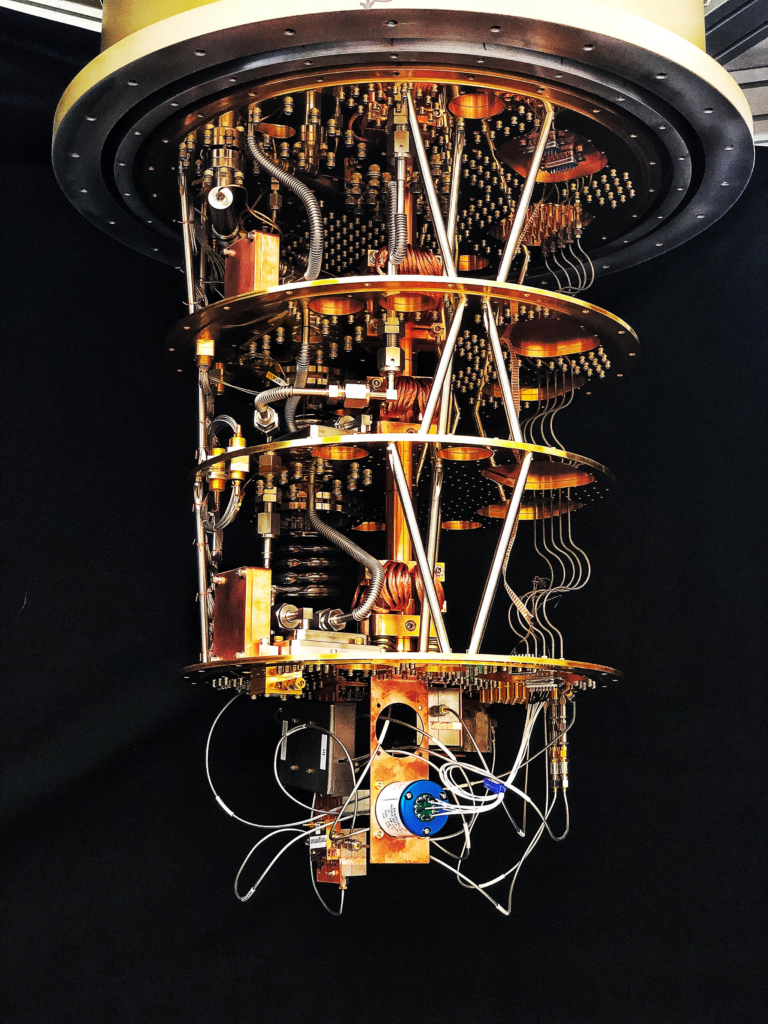

The reason quantum computing drives this demand is physics. Dilution refrigerators, the cooling systems that bring quantum processors down to temperatures around 10 millikelvin, use helium-3 as their working fluid. There is no credible substitute at present. Every dilution refrigerator running a quantum computer needs a continuous supply of helium-3. As the number of quantum computers globally moves from hundreds to thousands and eventually tens of thousands, the supply question becomes structural, not academic.

The Moon, meanwhile, has been accumulating helium-3 for billions of years through solar wind bombardment. The isotope is embedded in lunar regolith across the surface in concentrations that are modest by terrestrial mining standards, but enormous relative to what Earth’s stockpiles can provide. Whether extraction is at a useful scale, and is technically and economically viable, is precisely the question Interlune is building toward answering.

| Rabbt Research Deep-dive analysis on frontier economy companies. Structural position, dependency mapping, and what to watch, before the narrative forms. Subscribe at rabbt.substack.com |

Interlune: Owning the Resource, the Mission, and the Bridge

Private. Founded 2020, Seattle. Total disclosed funding: approximately $23M including $18M seed (2024), a $5M SAFE offering (January 2026), and multiple government grants from NASA, NSF, and the DOE. Co-founders: Rob Meyerson (CEO, former Blue Origin president) and Dr. Harrison Schmitt (the only geologist to have walked on the Moon, Apollo 17).

Interlune’s structural position is unusual. The company has secured commercial commitments from customers before extraction technology has been demonstrated on the lunar surface, before a single mission has returned material, and before the price per liter has been tested at volume. The purchase orders are there because the customers cannot wait for the supply chain to be fully proven before locking in a position. Bluefors, for instance, needs certainty about helium-3 availability years in advance to plan manufacturing capacity. That urgency gives Interlune negotiating leverage that most early-stage resource companies do not have.

The roadmap runs in three phases. The first, the Crescent Moon mission, is already in motion. Interlune’s multispectral camera, developed with NASA’s Ames Research Center, has been integrated onto Astrolab’s FLIP rover, which will fly to the lunar south pole on Astrobotic’s Griffin-1 lander, targeted for late 2026. The camera identifies ilmenite concentrations in regolith as a proxy for helium-3 presence, providing the first in-situ prospecting data for a commercial resource program. The second phase, Prospect Moon, is the extraction demonstration mission now under the $6.9 million NASA contract, targeting 2028. The third phase, Harvest Moon, is designed for full-scale extraction and return in the early 2030s.

The bridge strategy is what makes the 2028 delivery commitment credible, or at least less implausible than it initially appears. Interlune is also developing a terrestrial extraction process, using cryogenic separation to pull trace helium-3 from industrial-grade helium supplies. That process is intended to serve customers in the near term while the lunar program matures. The AFWERX contract awarded in late 2025 funds that work specifically for national security customers. If the terrestrial bridge yields meaningful volume, Interlune can begin serving Maybell Quantum and other customers before the first lunar return mission lands.

The key dependencies are layered. The entire prospecting timeline depends on Griffin-1 launching successfully and Astrolab’s FLIP rover operating as designed on the south polar surface. The 2028 extraction demonstration depends on the Prospect Moon payload passing flight qualification by Fall 2027 per the NASA contract terms. The commercial deliveries depend on the terrestrial bridge producing enough volume to meet initial contract obligations while the full lunar program catches up. Each of those dependencies has its own execution risk, and they are sequential, not parallel.

What to watch: Whether the Crescent Moon camera returns usable concentration data from Griffin-1, which would be the first real prospecting validation; and whether the Prospect Moon payload meets its Fall 2027 integration deadline. A slip in either milestone compresses the already tight path to 2028 delivery commitments.

Who Buys It and Why the Dependency Is Structural

Bluefors, headquartered in Helsinki, is the world’s leading manufacturer of dilution refrigerators. Its systems cool quantum computers to the sub-10-millikelvin temperatures required for stable qubit operation. The company has committed to purchasing up to 10,000 liters of lunar helium-3 annually from Interlune between 2028 and 2037, a volume that reflects the scale of the quantum compute buildout Bluefors is anticipating.

However, Bluefors is not a passive buyer waiting for supply to arrive. The company is simultaneously investing in alternative cooling architectures, including work on systems that reduce helium-3 consumption. That is a rational hedge. If helium-3 delivery timelines slip, Bluefors cannot afford to have its product roadmap dependent on a single lunar startup. The structural tension here is real: Interlune needs Bluefors as a credible anchor customer to validate the business model, while Bluefors needs Interlune to solve a supply problem it cannot solve through any other current channel. Each is dependent on the other in ways neither fully controls.

Maybell Quantum, based in Colorado, has positioned itself as a next-generation cryogenic infrastructure company. Its dilution refrigerators support three times the qubit density of competing systems at one-tenth the physical footprint, which matters enormously as quantum computing labs try to scale from experimental rigs to production-grade installations. Maybell’s first commercial order for helium-3 from Interlune, announced in May 2025, was specifically tied to fueling that scaling path. The company’s CEO has publicly framed the demand picture: a shift from a few hundred quantum computers worldwide to thousands, then tens of thousands, each requiring continuous helium-3 supply for operation.

Neither Bluefors nor Maybell Quantum is publicly traded. Market context therefore comes from the broader quantum computing sector and the cryogenics supply chain rather than individual company financials. The IEA has warned that helium shortages could delay quantum computing adoption by two to three years. That framing matters: the supply constraint is not hypothetical, and the structural deficit of 20,000 to 40,000 liters per year identified by current industry analysis is already a live operational problem for dilution refrigerator manufacturers, not a future concern.

Comparison: The Lunar Helium-3 Stack

| Company | Role in Stack | Structural Position | Key Dependency | What to Watch |

| Interlune (Private) | Helium-3 resource extraction, lunar and terrestrial | Controls the only near-term commercial pipeline for lunar He-3. Owns resource rights, extraction IP, customer contracts, and mission roadmap. | Astrobotic Griffin-1 launch success; 2028 first delivery window; terrestrial extraction yield from Grade A helium | Prospect Moon payload integration by Fall 2027; Crescent Moon camera data from Griffin-1 late 2026; whether letters of intent convert to binding contracts beyond current $500M |

| Bluefors (Private, Helsinki) | Dilution refrigerator manufacturer; largest He-3 consumer in quantum sector | Controls the cryogenic cooling layer that quantum computers depend on. Committed to 10,000 liters/year from Interlune 2028-2037. | Helium-3 supply availability on schedule; alternative cooling technology development (cADR) from competitors such as Kiutra | Whether 2028 delivery commitment triggers contingency sourcing; Bluefors’ own R&D into helium-3-lean refrigeration architectures |

| Maybell Quantum (Private, Colorado) | Quantum cryogenic infrastructure; Interlune’s first named commercial customer | Compact dilution refrigerator design supports higher qubit density. Positioned as critical infrastructure for quantum compute scale-out. | Helium-3 delivery from Interlune starting 2029; quantum computing adoption pace driving refrigerator demand | Whether 2029 delivery window holds; Maybell’s customer pipeline growth as a proxy for sector-wide He-3 demand |

The Honest Tension

The purchase commitments are real. The supply chain to fulfill them is not. Interlune has $500 million in binding orders and a mission architecture designed to make delivery possible by 2028. However, the terrestrial bridge, which is the mechanism for meeting near-term commitments, depends on cryogenic separation from industrial helium yielding meaningful helium-3 volume at competitive cost. That process has not been demonstrated at commercial scale. The lunar program, additionally, depends on at least two missions operating successfully before any material returns to Earth. Griffin-1 could slip. Prospect Moon could slip. And even if both proceed on schedule, the full Harvest Moon extraction mission that would supply volume at scale is currently targeted for the early 2030s, which means the period between 2028 and that date requires the terrestrial bridge to carry substantially more weight than the lunar program alone. The customers have bet on Interlune. The question is whether the bridge and the lunar timeline are robust enough to honor those bets without a renegotiated delivery schedule.

| Rabbt Intelligence Note A structured Research File on Interlune would map the gap between binding purchase order commitments and actual delivery timelines against the terrestrial extraction bridge strategy, and flag the 2028 first-delivery window as the condition most likely to reveal whether that bridge holds under commercial pressure. The Relationship Graph would show that Bluefors and Maybell Quantum are not just customers, they are structural dependencies on the supply side of an industry Interlune is simultaneously trying to establish, a circular positioning that most coverage of the lunar economy narrative misses entirely. The open question: if terrestrial helium-3 extraction from Grade A industrial helium scales faster than expected, does that undercut the urgency of the lunar program or validate it by proving the market is real? |

0 Comments